Featured

Table of Contents

Many agreements allow withdrawals listed below a specified level (e.g., 10% of the account worth) on an annual basis without surrender charge. Buildup annuities usually supply for a money repayment in the event of death prior to annuitization.

The agreement might have a stated annuitization date (maturation day), yet will usually allow annuitization any time after the very first year. Annuity income alternatives detailed for instant annuities are usually also readily available under delayed annuity contracts. With a buildup annuity, the contract owner is said to annuitize his/her accumulation account.

What happens if I outlive my Annuity Income?

You can make a partial withdrawal if you require added funds. On top of that, your account value continues to be kept and attributed with current interest or investment revenues. Certainly, by taking regular or methodical withdrawals you risk of depleting your account value and outliving the contract's accumulated funds.

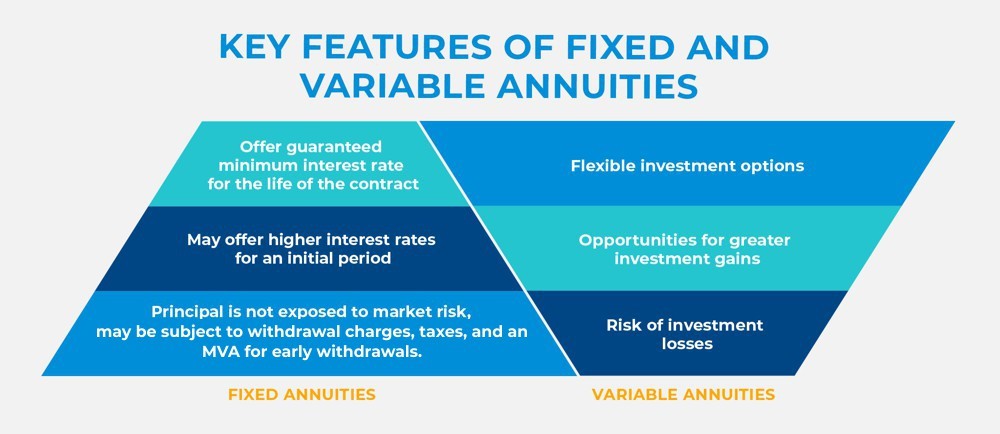

In the majority of agreements, the minimum rate of interest is evaluated issue, but some contracts allow the minimal price to be adjusted regularly. Excess interest agreements offer flexibility relative to premium repayments (single or adaptable) (Senior annuities). For excess passion annuities, the maximum withdrawal cost (additionally called a surrender cost) is topped at 10%

A market worth adjustment adjusts an agreement's account worth on surrender or withdrawal to mirror adjustments in rate of interest since the receipt of agreement funds and the remaining duration of the interest rate assurance. The change can be favorable or adverse. Fixed indexed annuities. For MGAs, the maximum withdrawal/surrender charges are shown in the adhering to table: Year 1Year 2Year 3Year 4Year 5Year 6Year 7Year 8 and Later7%6%5%4%3%2%1%0%Like a deposit slip, at the expiry of the warranty, the accumulation quantity can be restored at the firm's brand-new MGA rate

What is the best way to compare Lifetime Payout Annuities plans?

Unlike excess passion annuities, the amount of excess rate of interest to be credited is not recognized up until completion of the year and there are usually no partial credit scores during the year. The technique for determining the excess rate of interest under an EIA is determined in breakthrough. For an EIA, it is essential that you understand the indexing features used to identify such excess interest.

You should also understand that the minimal flooring for an EIA differs from the minimum flooring for an excess rate of interest annuity. In an EIA, the floor is based upon an account value that might credit a lower minimum interest price and may not credit excess passion every year. In enhancement, the maximum withdrawal/surrender fees for an EIA are set forth in the adhering to table: Year 1Year 2Year 3Year 4Year 5Year 6Year 7Year 8Year 9Year 10Year 11 and Later10%10%10%9%8%7%6%5%4%3%0% A non-guaranteed index annuity, additionally commonly described as an organized annuity, registered index linked annuity (RILA), buffer annuity or floor annuity, is an accumulation annuity in which the account worth increases or decreases as figured out by a formula based upon an external index, such as the S&P 500.

The allocation of the quantities paid right into the contract is typically elected by the proprietor and may be transformed by the owner, based on any legal transfer limitations (Fixed-term annuities). The adhering to are very important features of and considerations in purchasing variable annuities: The contract owner births the investment danger linked with properties kept in a separate account (or sub account)

Withdrawals from a variable annuity may undergo a withdrawal/surrender charge. You ought to understand the dimension of the fee and the length of the surrender fee period. Beginning with annuities marketed in 2024, the maximum withdrawal/surrender fees for variable annuities are set forth in the complying with table: Year 1Year 2Year 3Year 4Year 5Year 6Year 7Year 8 and Later8%8%7%6%5%4%3%0%Request a copy of the program.

Annuity Investment

Most variable annuities include a death benefit equivalent to the higher of the account value, the costs paid or the greatest wedding anniversary account value. Numerous variable annuity agreements use assured living advantages that give a guaranteed minimum account, earnings or withdrawal benefit. For variable annuities with such ensured advantages, consumers ought to be conscious of the fees for such advantage guarantees along with any kind of constraint or restriction on investments alternatives and transfer rights.

For dealt with delayed annuities, the bonus offer price is included to the rate of interest stated for the very first agreement year. Know how much time the bonus offer price will be credited, the rate of interest to be credited after such bonus rate period and any kind of surcharges attributable to such bonus, such as any higher surrender or death and cost fees, a longer surrender cost period, or if it is a variable annuity, it might have an incentive regain cost upon death of the annuitant.

In New york city, agents are called for to give you with contrast kinds to assist you choose whether the substitute remains in your finest interest. Be aware of the repercussions of replacement (brand-new abandonment cost and contestability period) and make certain that the brand-new product matches your present needs. Watch out for changing a postponed annuity that can be annuitized with a prompt annuity without comparing the annuity settlements of both, and of replacing an existing contract entirely to obtain a reward on an additional product.

Income tax obligations on rate of interest and investment revenues in deferred annuities are deferred. In general, a partial withdrawal or abandonment from an annuity before the proprietor gets to age 59 is subject to a 10% tax fine.

How do I apply for an Annuity Contracts?

Normally, insurance claims under a variable annuity agreement would be satisfied out of such different account assets. Make certain that the agreement you choose is appropriate for your conditions. For instance, if you buy a tax qualified annuity, minimum circulations from the contract are required when you get to age 73 - Retirement income from annuities (Annuity accumulation phase). You need to recognize the influence of minimum distribution withdrawals on the guarantees and advantages under the contract.

Just purchase annuity items that match your needs and goals which are proper for your monetary and family scenarios. Ensure that the agent or broker is certified in good standing with the New York State Department of Financial Providers. The Division of Financial Services has embraced rules calling for agents and brokers to act in your best passions when making suggestions to you associated to the sale of life insurance policy and annuity items.

Be careful of an agent who suggests that you sign an application outside New york city to buy a non-New York item. Annuity items approved to buy in New york city normally provide higher consumer securities than items offered in other places. The minimal account values are higher, fees are reduced, and annuity settlements and survivor benefit are a lot more favorable.

What are the top Annuity Contracts providers in my area?

While doing so, that development can possibly experience growth of its own, with the gains worsening over time. The opportunity to attain tax-deferred development can make a significant difference in your income in retirement. A $100,000 acquisition payment intensified at a 5% price yearly for 20 years would certainly expand to $265,330.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Your Investment Choices Key Insights on Your Financial Future What Is Fixed Annuity Vs Equity-linked Variable Annuity? Advantages and Disadvantages of Different Retirement Plans Why Fixe

Decoding How Investment Plans Work Key Insights on Your Financial Future Breaking Down the Basics of What Is Variable Annuity Vs Fixed Annuity Advantages and Disadvantages of What Is A Variable Annuit

Analyzing Strategic Retirement Planning Key Insights on Your Financial Future Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Retirement Income Fixed Vs Variabl

More

Latest Posts