Featured

Table of Contents

Trustees can be household members, relied on people, or economic establishments, depending upon your choices and the complexity of the trust. Ultimately, you'll require to. Possessions can include cash money, property, stocks, or bonds. The objective is to make sure that the count on is well-funded to meet the youngster's long-term economic requirements.

The role of a in a youngster support trust can not be understated. The trustee is the individual or company liable for handling the count on's assets and ensuring that funds are dispersed according to the terms of the trust agreement. This consists of seeing to it that funds are utilized exclusively for the child's advantage whether that's for education, clinical treatment, or everyday expenditures.

They must also give normal reports to the court, the custodial parent, or both, depending upon the regards to the count on. This accountability guarantees that the count on is being taken care of in such a way that advantages the child, avoiding misuse of the funds. The trustee additionally has a fiduciary responsibility, meaning they are legitimately bound to act in the most effective rate of interest of the youngster.

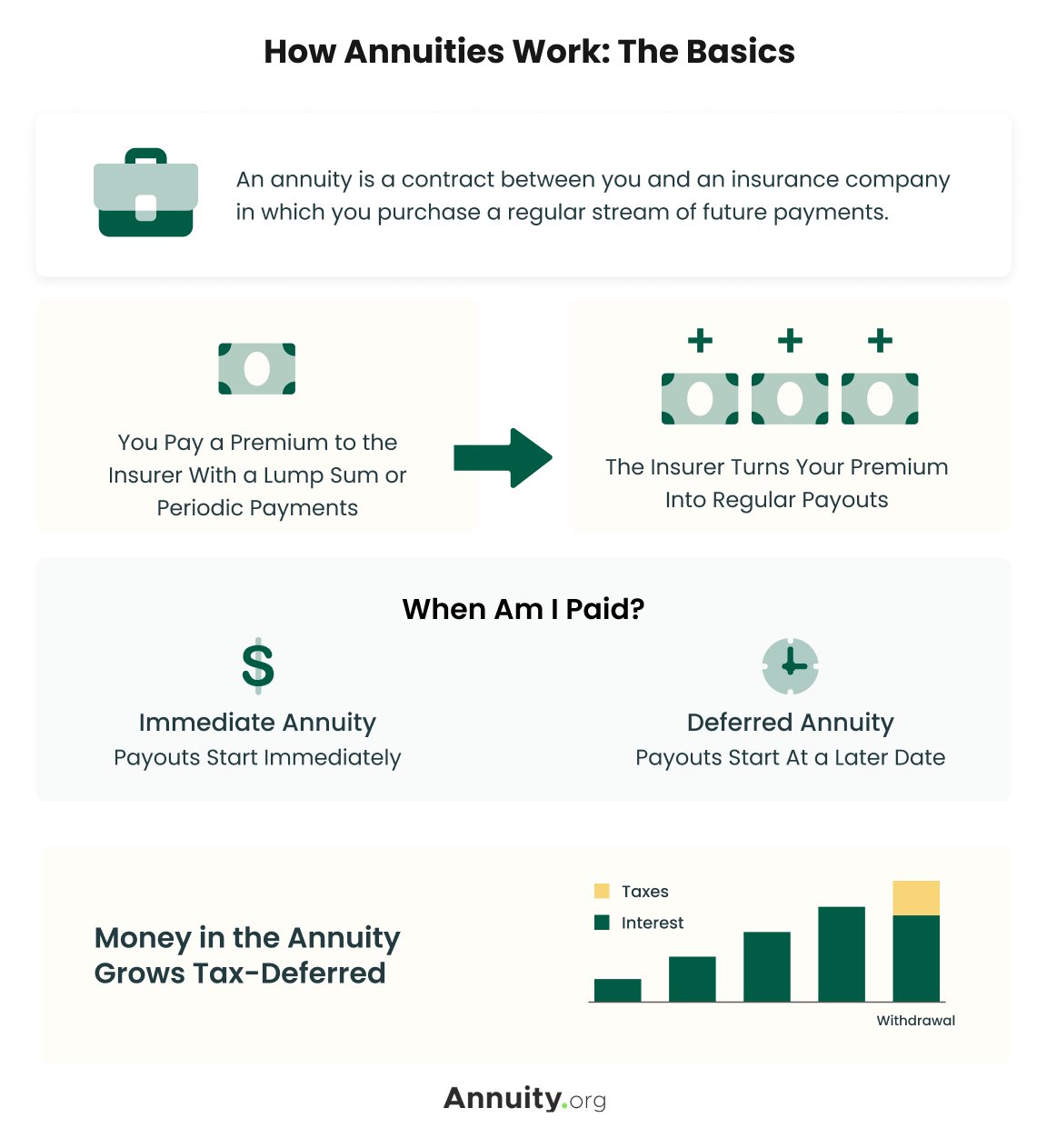

By buying an annuity, moms and dads can make certain that a fixed amount is paid out regularly, despite any kind of fluctuations in their earnings. This provides satisfaction, recognizing that the youngster's needs will certainly continue to be met, regardless of the economic scenarios. Among the key benefits of utilizing annuities for youngster assistance is that they can bypass the probate process.

How much does an Tax-deferred Annuities pay annually?

Annuities can likewise supply security from market fluctuations, ensuring that the kid's monetary assistance continues to be stable even in unstable economic problems. Annuities for Child Support: An Organized Service When establishing, it's important to think about the tax obligation ramifications for both the paying parent and the child. Trust funds, relying on their framework, can have various tax obligation treatments.

In other situations, the beneficiary the youngster may be accountable for paying taxes on any kind of distributions they receive. can likewise have tax obligation implications. While annuities offer a stable revenue stream, it is very important to recognize how that earnings will be strained. Depending on the structure of the annuity, settlements to the custodial moms and dad or youngster might be taken into consideration gross income.

One of the most substantial benefits of utilizing is the ability to shield a child's financial future. Trust funds, particularly, use a degree of defense from creditors and can make certain that funds are utilized properly. A count on can be structured to ensure that funds are only utilized for details functions, such as education or medical care, avoiding abuse.

Can I get an Income Protection Annuities online?

No, a Texas youngster support depend on is specifically designed to cover the kid's essential demands, such as education and learning, health care, and daily living expenses. The trustee is legally obliged to guarantee that the funds are utilized only for the benefit of the child as outlined in the depend on agreement. An annuity supplies structured, foreseeable payments over time, guaranteeing consistent monetary support for the youngster.

Yes, both youngster support trusts and annuities come with potential tax implications. Depend on earnings may be taxed, and annuity repayments might also be subject to taxes, depending on their structure. Considering that lots of seniors have been able to conserve up a nest egg for their retired life years, they are commonly targeted with fraudulence in a means that younger people with no cost savings are not.

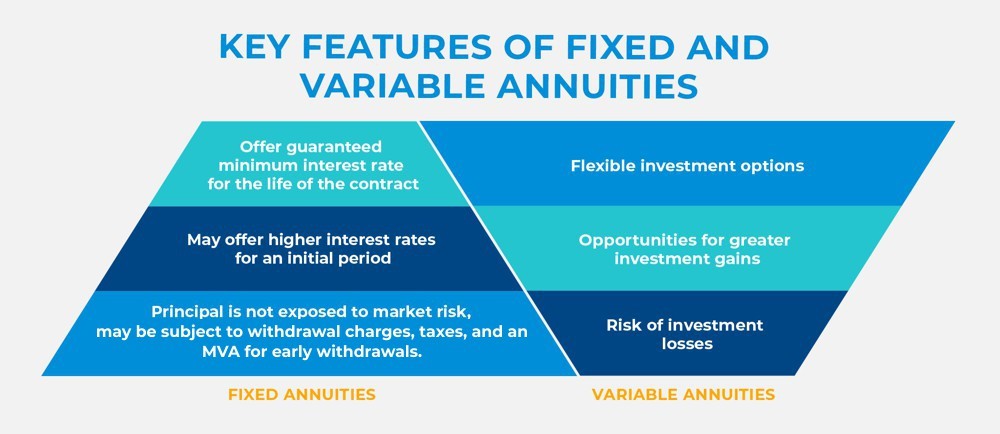

In this setting, customers must equip themselves with info to protect their rate of interests. The Chief law officer offers the adhering to pointers to consider before acquiring an annuity: Annuities are difficult financial investments. Some bear complicated top qualities of both insurance coverage and securities products. Annuities can be structured as variable annuities, taken care of annuities, instant annuities, postponed annuities, and so on.

Customers should review and understand the syllabus, and the volatility of each financial investment listed in the prospectus. Capitalists should ask their broker to describe all terms in the prospectus, and ask concerns regarding anything they do not understand. Fixed annuity products might additionally lug threats, such as long-term deferment durations, disallowing capitalists from accessing every one of their money.

The Attorney general of the United States has filed lawsuits versus insurer that sold improper deferred annuities with over 15 year deferment durations to financiers not anticipated to live that long, or who need accessibility to their cash for healthcare or helped living costs (Annuity withdrawal options). Financiers ought to make certain they know the long-term consequences of any type of annuity purchase

Who has the best customer service for Annuity Interest Rates?

Be careful of workshops that use complimentary meals or presents. In the long run, they are hardly ever free. Be careful of agents who give themselves phony titles to enhance their reliability. The most considerable charge connected with annuities is typically the abandonment cost. This is the percent that a consumer is billed if he or she withdraws funds early.

Customers might desire to consult a tax obligation professional prior to buying an annuity. Furthermore, the "safety and security" of the financial investment relies on the annuity. Be careful of agents that aggressively market annuities as being as secure as or far better than CDs. The SEC cautions consumers that some sellers of annuities items advise consumers to switch over to an additional annuity, a technique called "spinning." Sadly, agents may not appropriately reveal charges linked with switching financial investments, such as brand-new abandonment fees (which commonly begin again from the day the product is changed), or considerably modified benefits.

Agents and insurance coverage firms might offer bonuses to entice capitalists, such as extra rate of interest factors on their return. The benefits of such "incentives" are commonly surpassed by increased charges and management prices to the capitalist. "Bonuses" might be just marketing tricks. Some underhanded agents urge consumers to make impractical investments they can not afford, or purchase a long-lasting deferred annuity, although they will require accessibility to their cash for healthcare or living costs.

This section gives information useful to senior citizens and their households. There are lots of occasions that could influence your benefits. Gives information frequently asked for by brand-new senior citizens including changing wellness and life insurance policy choices, Sodas, annuity settlements, and taxable sections of annuity. Explains exactly how benefits are impacted by events such as marriage, separation, fatality of a spouse, re-employment in Federal solution, or failure to manage one's funds.

Who provides the most reliable Annuity Riders options?

Trick Takeaways The recipient of an annuity is an individual or organization the annuity's owner assigns to receive the contract's fatality benefit. Various annuities pay to beneficiaries in different methods. Some annuities might pay the beneficiary constant payments after the agreement holder's death, while other annuities might pay a survivor benefit as a round figure.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Your Investment Choices Key Insights on Your Financial Future What Is Fixed Annuity Vs Equity-linked Variable Annuity? Advantages and Disadvantages of Different Retirement Plans Why Fixe

Decoding How Investment Plans Work Key Insights on Your Financial Future Breaking Down the Basics of What Is Variable Annuity Vs Fixed Annuity Advantages and Disadvantages of What Is A Variable Annuit

Analyzing Strategic Retirement Planning Key Insights on Your Financial Future Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Retirement Income Fixed Vs Variabl

More

Latest Posts